Who will care? Risks of making vaccination a condition of deployment in homecare

Findings from a new survey of homecare providers

A public consultation on introducing vaccination as a condition of deployment across health and social care closed on 22 October 2021 and the Government is still considering its response.

At the Homecare Association we strongly support vaccination of careworkers. We lobbied hard, right from the beginning, to ensure it was as easy as possible for homecare staff to be vaccinated.

We understand that people receiving services may expect careworkers to be vaccinated and the benefits that vaccination brings in protecting against serious illness. However we are extremely concerned by the intention to legislate rather than persuade, in the current recruitment environment. Tens of thousands of older and disabled people who are reliant on support may find that no care is available for them. Who will care for them?

The Government must enable the sector to address workforce shortages and have a contingency plan for the care of older and disabled people before introducing such measures.

We asked our members what they thought the impact of vaccination as a condition of deployment might be. We had responses from 150 providers across England who provide care to almost 27,000 people and employ 33,500 staff. This includes providers that focus on state-funded care and providing care to people who fund their own care. The survey responses were received between 8 and 15 October 2021.

This is what they told us:

How would vaccination as a condition of deployment affect homecare?

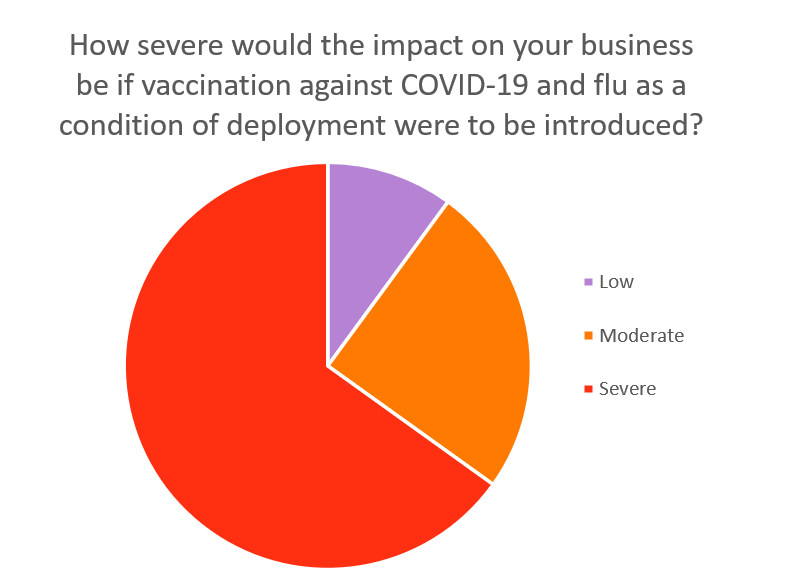

Two thirds (65%) of providers anticipated that the impact on their business would be severe if vaccination against COVID-19 and flu were required to deploy staff. 25% anticipated a moderate impact and 10% anticipated a low impact.

In terms of how it would affect providers:

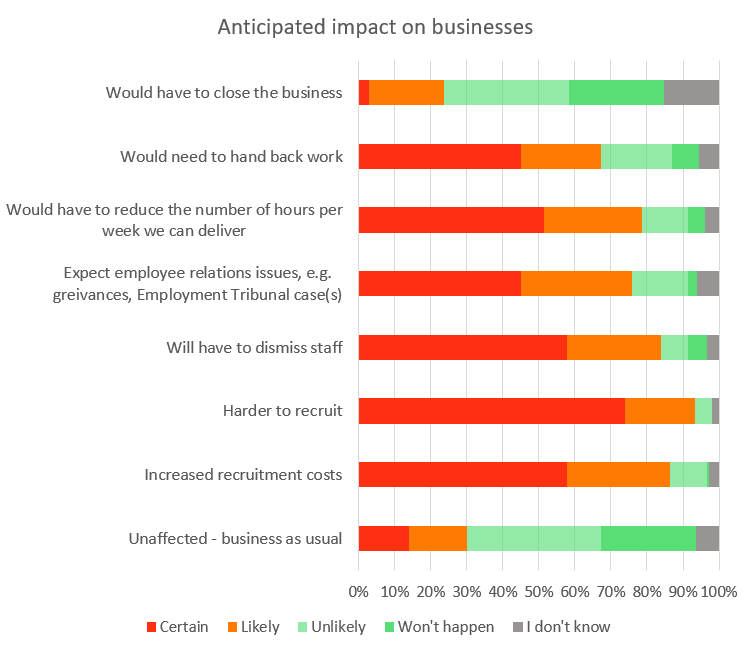

- 30% of providers thought it was certain or likely that they would be able to continue business as usual. 64% thought that business as usual was unlikely or would not happen.

- 86% of providers thought that it was certain or likely that there would be increased recruitment costs.

- 93% thought it was certain or likely that it would be harder to recruit (including 74% thinking this was certain).

- 84% thought it was certain or likely they would need to dismiss staff (including 58% who thought this was certain).

- 76% thought employee relations issues were certain or likely.

- 79% thought that it was certain or likely that they would have to reduce the number of hours per week delivered.

- 67% thought that it was certain or likely they would have to hand back work.

- 24% thought it was certain or likely that they would have to close the business.

- Both those focusing on the self-funded and publicly commissioned parts of the market were represented in businesses that thought it was certain or likely that they would need to reduce hours, or close the business due to the policy. However, businesses that relied on the state-funded part of the market were slightly more likely to think closure or reduction of hours delivered was certain or likely.

- Those businesses that thought it was certain or likely that they would close were spread across England and not only concentrated in one region.

Providers highlighted that, given they were operating at capacity, there was a direct relationship between hours delivered and staffing levels. Respondents were very concerned about not being able to recruit staff if careworkers left. In many cases a 20% reduction in staff would mean a 20% reduction in hours delivered. Even the loss of one or two care workers may mean that decisions would need to be made about reducing the number of people supported.

Other concerns about the impact on businesses included:

- Staffing: Providers are concerned about staffing shortages and rising recruitment costs. In some workplaces potential loss of colleagues or loss of trust could have significant impacts on morale and further staff shortages would increase pressures on remaining staff. Implementing the policy would also take its toll on service managers. There were concerns about how booster vaccines might impact recruitment in the long term.

- People using services: there were concerns about people losing services or carers with whom they had developed relationships. Existing waiting lists may get longer. Even services that don't hand back work may not be able to take on new clients. While some service users will feel safer and more confident in services if staff vaccination is required, not all service users supported vaccination requirements. Service providers reported receiving relatively low levels of enquiries about whether staff were vaccinated against COVID-19, and even less so in relation to flu.

- Financial viability: changes in immigration, fuel cost rises and other factors are increasing pressures on the sector. Rates paid by public sector commissioners are falling short of the cost of delivering care. Implementing the policy would involve extra administration and management costs when budgets are already stretched. Loss of staff might cause some businesses to consider reconfiguring/restructuring or selling the business. Restructuring could cause cash flow issues. The policy might reduce access to investment as well as limiting the ability for a business to break even or grow. Fee rates charged to clients that pay for their own care may need to be increased to cover costs. There were also concerns that discrimination and human rights cases could be taken against employers and what consequences these would have.

- Public reaction: there were concerns about the public understanding of the sector being adversely affected by the debate around vaccination. One provider raised concerns about comments from anti-vaxxers being made to them on social media.

- Relationships within the sector: there were concerns about staff being displaced to the unregulated part of the sector by this policy. There were also concerns about parity with the NHS and whether social care would be supported to cope with the legislation to the same degree as the NHS if the policy were implemented.

- Other points: it was felt that the Government needed to urgently address staffing issues in the sector now and not take action that could exacerbate the situation. There was a question over whether the focus on vaccines was disproportionate compared to PPE and testing. The lower prevalence of COVID-19 in homecare services compared to residential care settings was highlighted. There are a range of views amongst business owners and managers on vaccination. There were also concerns about GDPR compliance and potential impacts on CQC ratings.

Vaccination uptake

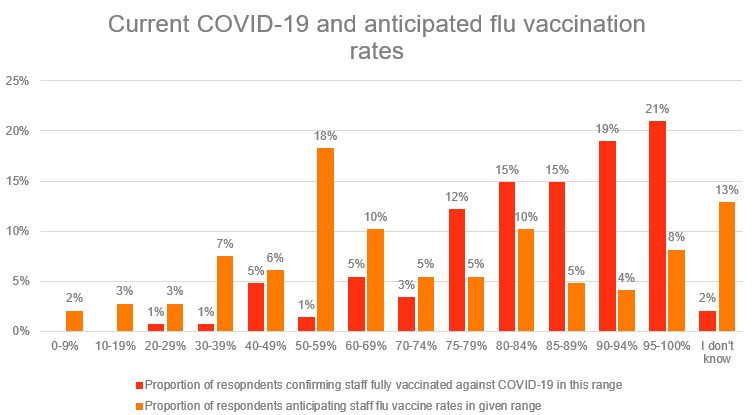

For COVID-19 40% of providers had 90% or more of their workforce fully vaccinated against COVID-19, 42% had 75-89% of their workforce vaccinated and 16% had less than three-quarters of their workforce vaccinated, with some reporting levels in the 20% range.

For flu vaccination the most common response was that providers expected about half of their workforce to be vaccinated. Only 12% were anticipating staff flu vaccination rates over 90% this winter. 20% reported in the 75-89% range. This is significantly lower than COVID-19 vaccination rates.

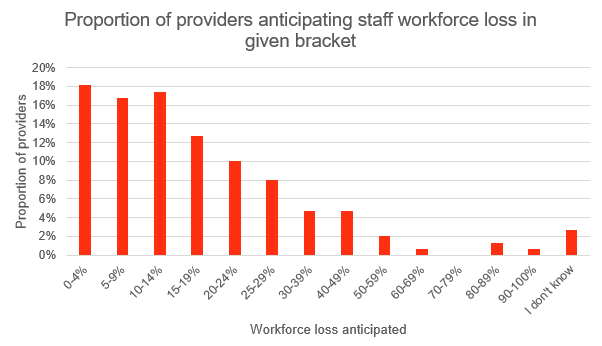

Anticipated workforce loss

If the COVID-19 vaccination was required for deployment in homecare then about a third of providers would expect to lose under 10% of their workforce. 40% reported that they would lose between 10 and 24% of their workforce. Almost a quarter (23%) thought they would lose a quarter or more of their workforce, with a minority expecting the majority of their staff would leave.

Of those reporting that they would lose 25% or more of their workforce all regions of England were represented apart from the South West. The North West, East of England and London were more strongly represented.

Of those reporting that they would lose 25% or more of their workforce, both business that focused more on self-funding and those that focused more on publicly commissioned business were represented. However, those that focused more on publicly commissioned business were slightly more strongly represented than in the total sample.

We received 130 responses to the question on the impact of the addition of flu vaccination to the requirements. 66% of providers thought that it would increase the number of staff who left. 18% felt it would not increase the number of staff who left. 15% found the outcome difficult to predict.

Those who did not expect the flu vaccination to worsen the situation (18%) tended to explain this through the fact that their vaccination rates were already high, or because the staff who were hesitant regarding the COVID-19 vaccine were the same as those that were hesitant about flu. Even amongst these providers, however, there were concerns about how this would affect recruitment and a lack of clarity about what new recruits may feel about the flu jab.

Providers who reported that they expected an increase (66%) felt that there were some staff who have had the COVID-19 vaccine who would not have the flu vaccine. There were concerns that the importance or urgency of the flu vaccine was not as widely accepted as the COVID-19 vaccine was, which may be seen in some ways as part of an exceptional response to the pandemic. In some cases the addition of the flu vaccine was felt to be one requirement too far.

The impact on individual providers would be likely to vary considerably (as with COVID-19) In some cases providers felt that the number of staff that would leave would increase by 50% or more if flu vaccination was mandatory.

If flu vaccine uptake were to mirror uptake in previous years (see also: anticipated uptake graph above), then a substantial proportion of the workforce would not meet the requirement.

Support received

Around a half of respondents had received support from local authorities (51%). 18% had received support from Public Health; 16% from the NHS; 11% felt they did not need support at this stage. Other sources of support mentioned were in-house support (for example from a head office) or support from a local care provider association.

Between a quarter and a third of providers did not believe any interventions were helping and that the underlying issues were people’s strongly held beliefs or level of trust in the Government which were unlikely to be changed.

Providers listed measures that had been successful for them, which included one to one and small group discussions; good communications using a variety of formats; being able to pay staff time to get vaccinated; and external factors such as staff seeing vaccination as being a benefit outside of work.